Financial shame creates anxiety and avoidance through nervous system responses that worsen financial situations over time, but evidence-based therapeutic interventions including trauma-informed care and graduated exposure techniques help individuals break the shame-avoidance cycle and develop healthier money relationships.

That paralyzing feeling when you avoid checking your bank account isn't about laziness or poor self-control. Financial shame triggers a nervous system response that makes your brain prioritize emotional protection over practical action, transforming temporary money stress into destructive long-term patterns.

What is financial shame? (And why it’s different from guilt)

When you forget to pay a bill on time, you might think, “I messed up.” That’s guilt. But when you look at your bank account and think, “I’m a failure,” that’s shame. The difference matters more than most people realize.

Financial shame is a deep, painful feeling that your money situation reflects something fundamentally wrong with you. It’s not about a single mistake or a bad decision. It’s a global self-assessment that attacks your identity and self-worth. While guilt says “I did something bad,” money shame whispers “I am bad.”

This distinction shapes everything about how you respond. Guilt tends to motivate action because your brain stays engaged in problem-solving mode. You feel bad about what happened, so you look for ways to fix it. Shame works differently. It triggers what researchers call a “dorsal vagal shutdown,” a nervous system response that makes you want to hide, freeze, or disappear. Your brain shifts from solving problems to protecting yourself from perceived threats to your identity.

The meaning of money shaming goes beyond personal feelings. It includes all the external messages you’ve absorbed about what your financial status says about your character. Maybe you heard “we don’t talk about money” growing up, or “people who struggle with money are lazy.” These messages become internalized beliefs that fuel shame long after the original comments fade from memory. Over time, financial shame can contribute to low self-esteem that extends far beyond your relationship with money.

What is toxic shame?

Toxic shame is shame that has become a core part of how you see yourself. Unlike healthy shame, which might briefly signal that you’ve violated your own values, toxic shame is persistent and pervasive. It convinces you that you’re fundamentally flawed, unworthy, or defective. When toxic shame attaches to money, every financial decision becomes evidence of your inadequacy. A declined credit card isn’t an inconvenience; it’s proof you don’t deserve good things.

What is financial anxiety?

Financial anxiety is the persistent worry, fear, or unease about money matters. It might show up as obsessive checking of your accounts, avoiding bills entirely, or physical symptoms like a racing heart when financial topics come up. While anxiety and shame are different experiences, they often travel together. Shame creates the belief that you’re bad with money, and anxiety keeps you hypervigilant about being “found out” or making another mistake that confirms your worst fears about yourself.

The hidden signs you’re carrying financial shame

Money shame rarely announces itself. It doesn’t show up as a clear thought like “I feel ashamed about my finances.” Instead, it disguises itself as anxiety, avoidance, or that familiar knot in your stomach when a bill arrives. Learning to recognize these hidden signs is a meaningful first step toward breaking free from their grip.

The tricky thing about financial shame is how normal it can feel. You might assume everyone dreads checking their bank balance or feels sick before talking about money with their partner. But these reactions often signal something deeper worth paying attention to.

Cognitive and emotional warning signs

Your thoughts and feelings offer some of the earliest clues that money shame has taken hold. On the cognitive side, you might notice catastrophic thinking patterns: one unexpected expense spirals into visions of bankruptcy, homelessness, or complete financial ruin. Your mind may actively avoid financial topics, changing the subject when friends discuss retirement plans or tuning out during money segments on the news.

The inner critic tends to get especially loud around spending decisions. Even reasonable purchases trigger harsh self-talk: “You’re so irresponsible. You’ll never get this right. What’s wrong with you?” This isn’t just being careful with money. It’s punishment.

Emotionally, financial shame creates responses that seem out of proportion to the situation. A $5 coffee purchase might trigger genuine distress. Conversations about money, even hypothetical ones, can spark panic or a sudden need to escape. When someone asks a simple question about your finances, you might feel a flash of defensiveness or anger that surprises even you. These intense stress responses signal that something beyond practical concern is at play.

Behavioral patterns that signal hidden shame

Actions often reveal what we’re unwilling to admit to ourselves. Financial shame drives specific behavioral patterns that become almost automatic over time.

Common avoidance behaviors include:

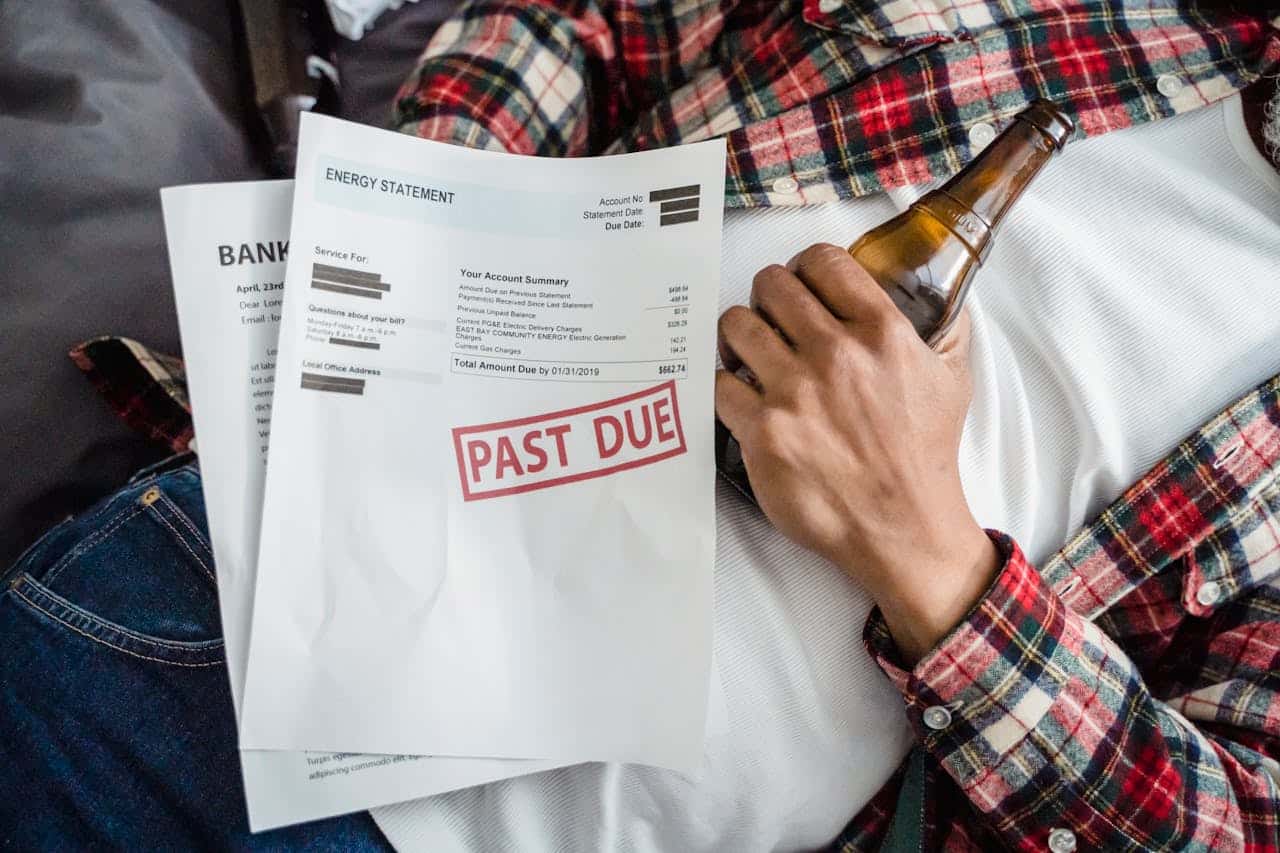

- Refusing to check bank accounts, sometimes for weeks or months

- Letting bills pile up unopened

- Procrastinating on financial tasks until they become emergencies

- Deleting banking apps or avoiding financial websites

Secrecy is another hallmark of money shame. You might hide purchases from your partner, removing tags or sneaking bags into the house. You could find yourself lying about how much something cost, either inflating prices to seem more successful or deflating them to avoid judgment. Financial secrecy in relationships often feels necessary for survival, even when you know it’s creating distance.

Physical and relational indicators

Your body keeps score of financial shame, even when your mind tries to ignore it. Pay attention to physical sensations like your stomach tightening when you open the mailbox, sweating or a racing heart when handing over a credit card, or lying awake the night before a financial conversation. These aren’t random. They’re your nervous system responding to perceived threat.

Financial shame also reshapes your relationships in subtle ways. You might avoid friends whose spending habits differ from yours, whether they have more or less money. Social invitations get declined because you can’t afford the restaurant or don’t want to explain why you’re ordering less. You withdraw from financial conversations with family, changing the subject or leaving the room.

In romantic relationships, money shame can create invisible walls. You might lie about your income, minimize your debt, or handle all finances alone to prevent your partner from seeing the full picture. These protective behaviors make sense in the moment, but they quietly erode trust and intimacy over time.

If you recognized yourself in several of these signs, you’re not alone. These patterns are common responses to financial shame, and naming them is a meaningful first step toward change.

The shame-avoidance-worsening cycle explained

Money shame rarely stays contained. Instead, it tends to feed on itself through a predictable pattern that makes financial situations progressively worse.

Stage 1: The trigger. Something activates your shame response. Maybe you open an unexpected medical bill, watch a friend buy a house while you’re still renting, or realize you overspent during a stressful week. The specific trigger matters less than what happens next in your brain and body.

Stage 2: Nervous system shutdown. Your body perceives the shame as a threat and responds accordingly. Heart rate increases, your stomach tightens, and your mind starts racing toward escape. This isn’t weakness or laziness. It’s your nervous system trying to protect you from what feels like an unbearable emotional experience.

Stage 3: Avoidance brings relief. You find ways to distance yourself from the painful feeling. You might stop opening bills, avoid checking your bank balance, lie to your partner about a purchase, or change the subject when friends discuss finances. In the moment, these behaviors work. The acute distress fades, and you can breathe again.

Intervention point: This is where awareness becomes powerful. Recognizing avoidance as a shame response, not a character flaw, creates space for different choices.

Stage 4: Real consequences accumulate. While avoidance provides emotional relief, it creates tangible problems. Bills become overdue. Late fees stack up. Debt grows silently. Opportunities for negotiation or assistance pass by. The financial situation that triggered shame in the first place gets measurably worse.

Intervention point: Small, supported actions here, like opening one piece of mail or checking one account, can prevent escalation.

Stage 5: Shame intensifies. When you finally confront the worsened situation, it seems to confirm everything you feared about yourself. “I really am terrible with money. I always mess this up.” This deepened shame makes future triggers even more activating, and the cycle spins faster.

Intervention point: Separating your financial behaviors from your worth as a person disrupts the shame narrative before it can take root again.

Each rotation through this cycle strengthens the pattern, but each stage also offers an opportunity to step off the track entirely.

Where financial shame comes from: childhood to present

Financial shame doesn’t appear out of thin air. It has roots, often stretching back further than you might realize. Understanding where your shame originated can help loosen its grip on your present-day financial life.

Your money scripts: childhood programming still running

Money scripts are unconscious beliefs about money that form during childhood and continue operating automatically in adulthood. You might not even know they’re there, but they shape every financial decision you make.

Think about your earliest money memories. Maybe you overheard your parents arguing about bills behind closed doors. Perhaps there was constant messaging about scarcity: “We can’t afford that” or “Money doesn’t grow on trees.” Or you might have received praise for saving every penny while spending was met with disappointment or punishment.

These experiences created internal rules you still follow today. A child who learned that wanting things meant being “greedy” may grow into an adult who feels guilty about any purchase, no matter how reasonable. Someone who witnessed financial chaos might develop rigid control around money, or avoid dealing with it altogether.

Your attachment patterns also play a significant role in how financial anxiety and shame show up. Early relational security, or the lack of it, shapes how safe you feel navigating uncertain situations like money management. If your emotional needs weren’t consistently met as a child, financial stress can trigger those same feelings of insecurity and unworthiness.

Socioeconomic trauma leaves lasting marks too. Growing up in poverty, experiencing sudden financial loss, or watching a parent lose their job can become formative shame experiences. These events teach children that financial instability equals personal failure, a lesson that’s hard to unlearn.

Inherited beliefs and generational patterns

Understanding the meaning of money shaming often requires looking at your family’s unspoken rules about finances. Every family has them: don’t talk about money, always appear successful, never ask for help, rich people are greedy, or poor people are lazy.

These beliefs get passed down like heirlooms, except no one consciously hands them over. You absorb them through observation, overheard comments, and emotional reactions. Your grandmother’s fear of debt becomes your mother’s anxiety, which becomes your avoidance.

Cultural backgrounds add another layer. Some cultures emphasize collective financial responsibility; others prize individual achievement. Neither is wrong, but the shame that comes from not meeting these expectations can be intense.

Present-day environments keep these childhood patterns alive. A critical partner, competitive coworkers, or social media highlight reels can all reinforce the old belief that you’re not measuring up. Your current shame often echoes something much older.

The 5 financial shame archetypes: which pattern fits you?

Money shame doesn’t look the same for everyone. The way you learned to cope with financial embarrassment shapes how it shows up in your daily life. Understanding your specific pattern can help you recognize when shame is driving your behavior, not logic or genuine preference.

These five archetypes represent common ways people protect themselves from the pain of financial shame. You might see yourself clearly in one, or notice pieces of yourself scattered across several.

The Hider

If you’re a Hider, secrecy is your primary shield. You might avoid opening bills, delete banking app notifications, or give vague answers when friends discuss money. The thought of anyone knowing your true financial situation feels unbearable.

Hiders often maintain two realities: the one they present to the world and the one they live with privately. This split takes enormous energy to sustain. You might feel relief when you successfully keep your finances hidden, but that relief is temporary. The underlying shame remains untouched, growing in the dark.

The Overcompensator

For Overcompensators, shame drives spending rather than saving. You might buy expensive items you can’t afford, pick up every check at dinner, or maintain an image of success that doesn’t match your bank account.

This pattern often develops when you’ve internalized the message that your worth depends on appearing financially successful. The painful irony is that overspending to mask shame typically creates more financial problems, which creates more shame. It’s a cycle that feeds itself.

The Self-Punisher

Self-Punishers use deprivation as a form of penance. If this is your pattern, you might deny yourself basic comforts or pleasures even when you can afford them. Deep down, you believe you don’t deserve financial security or enjoyment.

This archetype often develops after financial mistakes or during childhood experiences of scarcity. You might feel that suffering is the appropriate response to past money problems. Spending on yourself, even reasonably, triggers guilt rather than satisfaction.

The Comparer

Comparers measure their worth through constant financial comparison to others. No matter what you achieve, someone else always has more. You might obsessively track friends’ purchases, homes, or vacations, using their success as evidence of your own inadequacy.

Social media intensifies this pattern dramatically. The Comparer never feels “enough” because the goalposts keep moving. Financial decisions become less about your actual needs and more about keeping pace with an impossible standard.

The Frozen

If you’re Frozen, financial decisions feel paralyzing. You might leave money sitting in low-interest accounts for years, avoid negotiating salaries, or let important financial deadlines pass because choosing feels too risky.

The Frozen archetype develops when you’ve learned that financial mistakes lead to shame or punishment. Doing nothing feels safer than potentially getting it wrong. But avoidance has its own costs: missed opportunities, late fees, and the quiet stress of knowing important things remain undone.

Patterns shift and overlap

Most people don’t fit neatly into a single category. You might hide your debt while also overspending on visible items. You could freeze on investment decisions while punishing yourself by skipping small pleasures. These patterns can also shift over time or change depending on your stress level, relationships, or financial circumstances.

Recognizing your patterns isn’t about adding another layer of self-criticism. It’s about understanding the protective logic behind your behavior so you can start responding to money with awareness rather than automatic shame responses.